Note: This article’s statistics come from third-party sources and do not represent the opinions of this website.

The American dream is becoming just that for more and more people, as the real estate market is seeing fewer options and higher prices than ever before. Available homes fell by over 40% from 2019 to 2021. With the increase in demand and shortage in supply, obtaining a mortgage can be even more difficult now that lenders have the luxury of being more discerning with who they approve.

The mortgage is the key to the hopes and dreams of millions of aspiring homeowners. Yet while these massive loans remain highly coveted, there are many misconceptions surrounding how they work.

When you dig into the data, you see intriguing mortgage trends and insights worth noting. Here’s a look at mortgage and homeowner statistics that explore how home loans have evolved in America and what it means to apply for a mortgage this year.

Click below to jump ahead:

Top 12 Mortgage Statistics and Facts

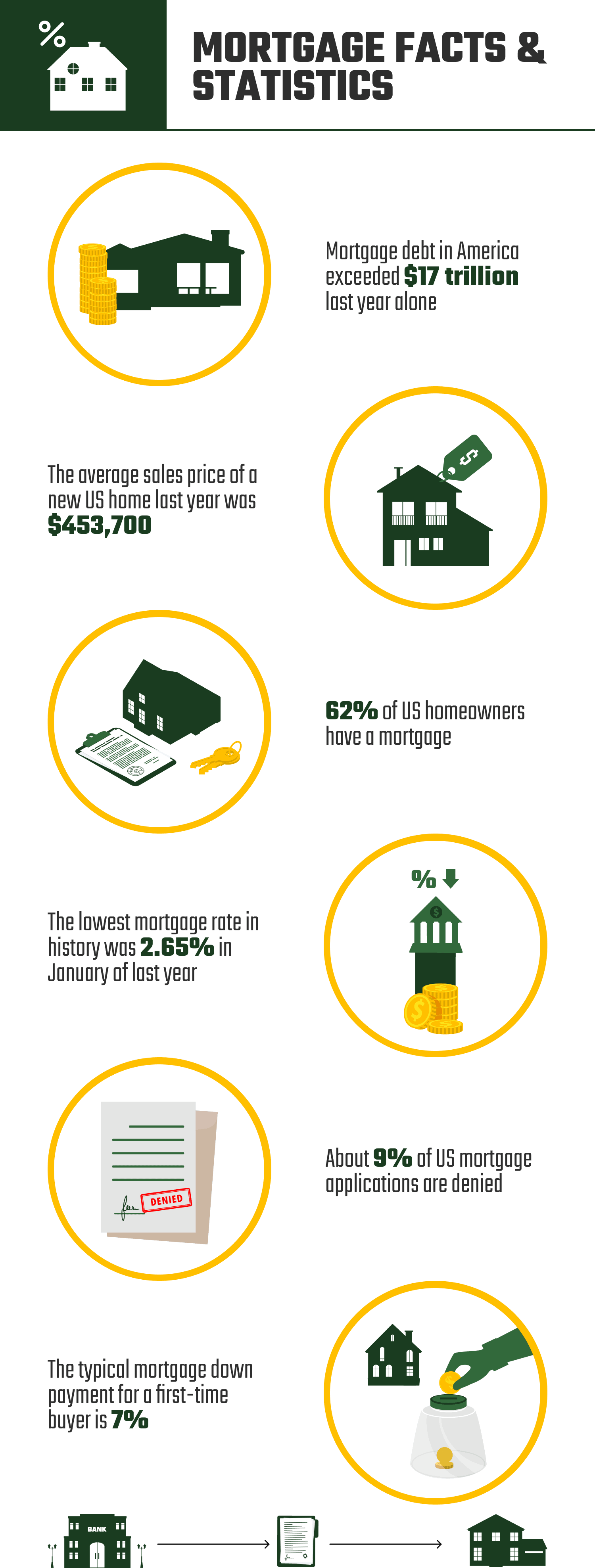

- Mortgage debt in America exceeded $17 trillion in 2021.

- The average sales price of a new home in 2021 was $453,700.

- The median mortgage value in 2020 was $251,700.

- 62% of homeowners have a mortgage.

- Refinancing mortgages outpaced purchases every quarter over the last two years.

- The lowest mortgage rate in history was 2.65% in January 2021.

- The highest mortgage rate in history was 18.63% in October 1981.

- The first American mortgages required a 50% down payment.

- About 9% of mortgage applications are denied.

- A high debt-to-income ratio is the number one reason for a mortgage application denial.

- The typical down payment for a first-time buyer is 7%.

- The average credit score used to get a mortgage in 2020 was 746.

Mortgages: The Current State

1. Mortgage debt in America exceeded $17 trillion in 2021.

(Statista)

Mortgage debt reached its highest point in 2021 when it totaled $17.6 trillion. The $82 billion increase from 2020, when mortgage debt was $16.78 trillion, is the highest single-year jump since 2007, one year before the housing crash.

2. The average sales price of a new home in 2021 was $453,700.

(Statista)

With rates at all-time lows, more people have been motivated to snatch up any leftover real estate, even if it means paying a higher price. It could be one reason the mortgage debt jumped so egregiously from 2020 to 2021.

From 2017 to 2020, home sale prices stayed relatively level, averaging $384,900–$392,000. It was the highest that prices had ever been, but the 5-year increase since 2015 was only $31,300. But in 2021, prices skyrocketed by $61,700 to an average total of $453,700 per home, indicating an increase in construction costs and an incredible willingness to overpay to take advantage of current rates.

3. The median mortgage value in 2020 was $251,700.

(U.S. Census Bureau)

Median mortgage values declined steadily after the housing crash. They hit their lowest point of the decade in 2014 at $193,500.

Since then, median values have increased year over year, with 2019–2020 showing the most significant jump yet. While median mortgage values only increased by $3,100 from 2014 to 2015, they grew by over $12,500 from 2019 to 2020.

4. 62% of homeowners have a mortgage.

(U.S. Census Bureau)

There were over 6 million existing home sales in 2021, the most since 2006. But interestingly, while home purchases are going up, the amount of Americans with mortgages is going down. The number of people with a mortgage in 2021 stood at 48,974,364, representing 62% of people with a home. That’s down from 2010, when 51,696,841 people had mortgages, making up 68% of all homeowners.

5. Refinancing mortgages outpaced purchases every quarter over the last two years.

(Statista)

Although purchases may have been at a 10-year high in recent years, refinancing has been the name of the home-loan-game since 2019. Every quarter since Q4 2019 has had a higher number of refinancing originations than purchase originations. The trend peaked in Q4 2020 when refinancing made up $851 billion worth of mortgage originations, compared to only $410 billion in purchases.

Purchases outpaced refinance loans for much of the 2010s. Recent low interest rates and high home values changed that by spurring so many homeowners to take advantage via rate refinancing.

In 2020, 45% of all home loans were for rate and term refinancing (FHFA). That’s a tremendous uptick since 2018, when refinancing of any kind, whether for lower interest rates or to cash out, only accounted for 34.4% of new mortgages. Only 12.4% of all originations were done to get better rates that year.

History of Mortgages

History of Mortgages

6. The lowest 30-year fixed mortgage rate in history was 2.65%.

(Freddie Mac)

We’re so used to everything getting more expensive that it may surprise some to find out that the lowest mortgage rate in history was rather recent. The rate on 30-year fixed mortgage rates hit an all-time weekly low in the first week of January 2021. That kicked off the best year overall for fixed mortgage rates in history, with 30-year fixed mortgages having an average of 2.96% interest and 15-year fixed rates averaging 2.27%.

7. The highest mortgage rate in history was 18.63%.

(Freddie Mac)

It may sound unthinkable, especially compared to today’s rate, but in one week in October of 1981, mortgage rates averaged 18.63%. Putting that in perspective, the monthly payment for a $100,000 mortgage with the lowest rate of 2.65% would be roughly $403 before taxes and fees. At 18.63%, that same amount would have a monthly payment, before taxes and fees, of $1,559!

The OPEC oil embargo from the 1970s takes most of the blame for the astronomical rates that year, which finished at an average of 16.63%. The embargo led to hyperinflation, which the Fed tried to fight via increased short-term interest rates. It worked out well for those with savings accounts, but it made much of the 1980s an expensive time to take out a loan.

8. The first American mortgages required a 50% down payment.

(How Stuff Works)

It seems like the concept has been around for ages, but the mortgage didn’t become an American economic staple until the 1930s. And the first ones were nowhere near as generous as what we have today.

As hard as it may be to get a mortgage in the current climate, the first mortgages only covered 50% of the home sale, meaning you had to have at least half the cash on hand to buy a house. Plus, while we have 15-, 20-, and 30-year options now, the earliest lenders gave you only about 5–7 years maximum to pay off your loan. With the short payoff periods and the onset of the Great Depression, it’s not surprising that as many as 50% of mortgages went into default in 1933.

Getting a Mortgage

9. About 9% of mortgage applications are denied.

(Consumer Financial Protection Bureau)

It’s uncommon for mortgage applications to be declined, as denial rates averaged about 9.3% from 2018 to 2020. FHA loans had the highest denial rates, and conventional conforming loans had the fewest at 7.6%.

10. A high debt-to-income ratio is the number one reason for a mortgage application denial.

(Oregon Live)

Denials may be infrequent, but they do happen. Many factors may lead to a declined application, including a poor credit score, low income, or limited work history. The driver of the most declines in 2020, however, was debt-to-income.

About 32% of mortgage denials stemmed from a high debt-to-income ratio in 2020. Most of those denials (85%) were for individuals with 60% or more DTI, while 21% had 50–60% DTI. Approval odds drastically increase when you have a DTI below 40%, and according to the stats, the best approval rates are for individuals with a DTI of 20–29%.

11. The typical down payment for a first-time buyer is 7%.

(National Association of Realtors)

One of the most persistent misconceptions among prospective homeowners is the amount of the down payment, which most are quick to overestimate. A 2020 National Association of Realtors survey found that 45% of individuals believed you needed to pay at least a 16% down payment or more before getting a home. At average costs of $391,900 that year, that would mean the typical house sale would require a down payment of at least $62,000!

Many loans require higher down payments to offset low credit scores and other limiting factors, but most first-time homebuyers pay less than 10% down. From 2018 to 2021, the standard down payment was only 6–7%. That was the highest average percentage since before the 2008 crash but still far below what many looking to buy a house expect to pay.

12. The average credit score used to get a mortgage in 2020 was 746.

(Federal Housing Finance Agency)

You don’t need perfect credit to buy a house, as the average in 2020 was 746 for all mortgages and 735 for first-time homebuyers. Those numbers may seem modest, but in reality, they’re the highest averages since the 1990s. The lowest credit rating for first-time homebuyers came in 2000 when people bought houses with an average score of 678.

The intense demand for the few houses left on the market is causing the average credit score to go up, as lenders can be pickier with approvals. Still, mortgage options exist for individuals with credit scores as low as 500. For example, FHA loans cater to individuals with scores in the 500–620 range, though these often come with higher minimum down payments and mortgage insurance requirements.

Frequently Asked Questions

What Is the Most Common Type of Mortgage?

With 90% of first-time homebuyer mortgages falling in the category, 20- and 30-year fixed rates mortgages are by far the most popular mortgage type. Interest rates like these don’t come around often, and as they start to climb, many people want a guaranteed low rate before they’re gone. For those refinancing, only 77% opted for longer terms, while 21% went with shorter 15-year terms.

What Is the Minimum Down Payment for Mortgages?

The minimum down payment for a mortgage depends on the lender and the type of loan. If you meet the credit requirements, you can get FHA loans with as little as 3.5% down, and some USDA and VA loans don’t require any down payment. Many banks and credit unions also offer unique loan packages featuring low/zero down payments and repayment options for associated fees. These are often geared toward first-time homebuyers to facilitate the purchase.

How Much Does the Average Mortgage Cost?

The average loan amount in 2020 was $286,000 for home purchases and $294,000 for refinancing loans. Mortgages increase every year and given the extreme increase in sale prices in 2021, it’s likely that the average loan for last year exceeded $300,000.

How Long Does It Take to Approve a Mortgage Application?

It only takes a few minutes to apply for a mortgage pre-approval online, and you generally get your pre-approved amount in 1–3 days. But to get the final approval for a loan, you may have to wait up to 30 days or longer for underwriting to cull through all of the information they need to make sure you qualify. They look at credit history, employment, savings and income, and a host of other variables before finalizing the mortgage.

Conclusion

As the cost of living continues its rise, more individuals are determined to buy homes, earn equity, and escape uncertain rental prices. We may never see rates like those in 2020–2021, but as they start their slow and steady upward movement, it’s still a great time to pursue a locked-in rate. With new home construction starting to get back on track and the market starting to cool, hope is on the horizon for individuals trying to secure a legacy with a new home and low-interest mortgage.

See Also:

Featured Image Credit: Jirsak, Shutterstock

Contents